Step-by-Step Strategy for Indians & Global Readers Earning Just ₹75K/month ($1K) to Become 100% Debt-Free

Stuck under a mountain of debt with barely enough income to survive? You’re not alone—and there’s a way out.

Debt doesn’t discriminate by geography. Whether you’re in Mumbai or Manhattan, Bangalore or Boston, the weight of financial obligations can feel crushing when your income barely covers your basic needs. But here’s the truth that debt collectors don’t want you to know: even with a modest income, you can systematically eliminate substantial debt.

This comprehensive guide is crafted specifically for those earning around ₹75,000 per month (approximately $900-1,000) while facing ₹12,00,000 (12 lakhs or about $15,000) in debt. We’ll provide practical strategies that work regardless of which currency you earn or which country you call home.

The Reality of Debt on a Limited Income

Before diving into solutions, let’s acknowledge the reality of your situation:

A Snapshot of Your Financial Reality

For Indian Readers:

- Debt Load: ₹12,00,000 (12 lakhs)

- Monthly Income: ₹75,000 (before tax)

- Typical Fixed Expenses:

- Rent: ₹20,000-25,000

- Food: ₹10,000-15,000

- Transportation: ₹5,000-8,000

- Current Loan EMIs: ₹25,000-30,000

- Utilities: ₹5,000-7,000

For International Readers:

- Debt Load: $15,000

- Monthly Income: $900-1,000 (before tax)

- Typical Fixed Expenses:

- Rent: $300-400

- Food: $150-200

- Transportation: $70-100

- Current Loan Payments: $300-400

- Utilities: $80-120

These numbers create a sobering picture: after essential expenses, there’s precious little left to tackle your debt. In many cases, you might even be operating at a small monthly deficit, watching your debt grow despite your best efforts.

The Emotional Toll

Beyond the numbers, there’s the constant anxiety, the sleepless nights, and the strain on relationships. Financial stress is among the most pervasive forms of chronic stress, and its effects extend far beyond your bank account.

One survey respondent from Chennai shared: “I avoided family gatherings because I couldn’t bear the shame of admitting I couldn’t afford gifts or contribute to celebrations. My debt became a prison, not just financially, but socially.”

This isolation is just one of many emotional burdens that accompany financial hardship. But remember this: your debt does not define your worth, and temporary financial challenges don’t determine your ultimate potential.

Your 36-Month Debt Freedom Roadmap

The path to financial freedom requires a systematic approach divided into four distinct phases:

- Immediate Survival (0-3 months): Stop the bleeding

- Stabilization (3-6 months): Create breathing room

- Debt Attack (6-18 months): Strategically eliminate balances

- Financial Freedom (18-36 months): Build security and prevent recurrence

Let’s break down each phase with specific, actionable steps tailored to your income level.

Phase 1: Immediate Survival (0-3 Months)

This crucial first phase is about stopping the financial bleeding and creating a minimum viable financial plan. The goal isn’t yet to make significant progress on debt repayment, but rather to stabilize your situation and prevent further damage.

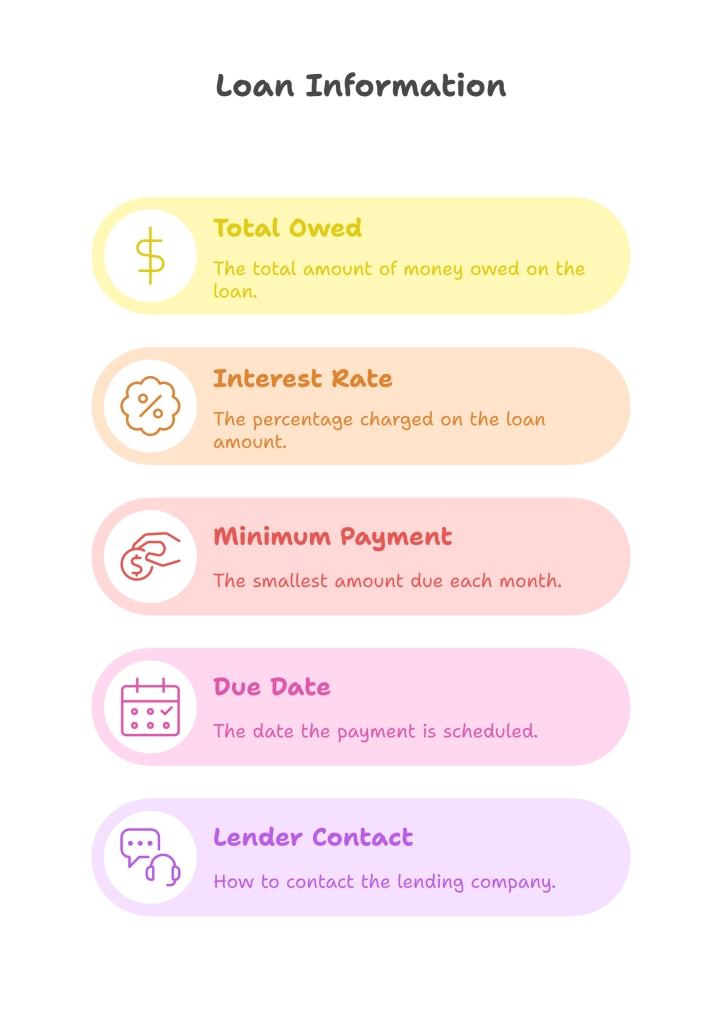

1. Perform a Complete Financial Inventory

Action Step: Create a detailed list of all debts with the following information:

- Total amount owed

- Interest rate

- Minimum monthly payment

- Due date

- Lender contact information

For Indian Context: Credit card debt (often 36-42% annual interest) Personal loans (12-24% annual interest) Home loans (7-9% annual interest) Vehicle loans (8-12% annual interest) Education loans (8-15% annual interest)

Subscribe to continue reading

Subscribe to get access to the rest of this post and other subscriber-only content.